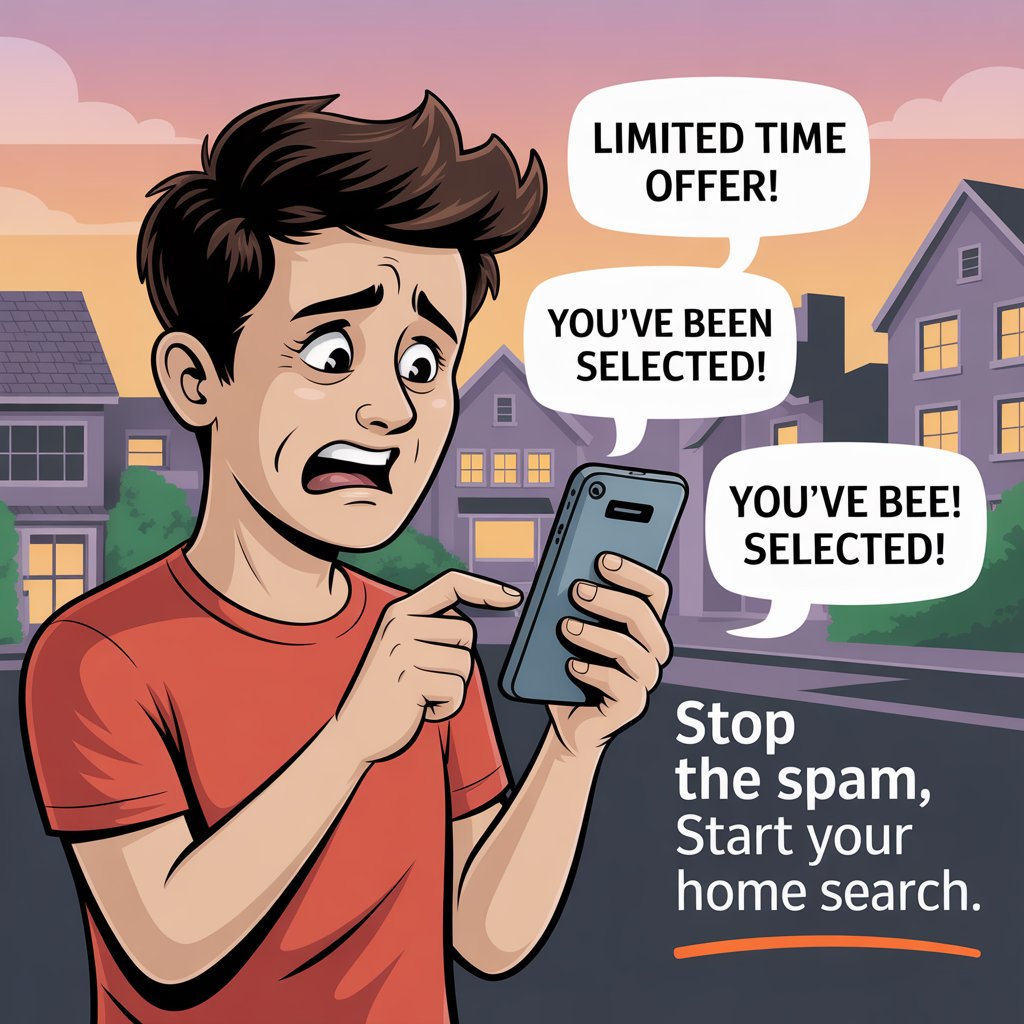

If you’ve recently checked your credit for a home loan and now your phone won’t stop buzzing with random calls and texts—welcome to the not-so-wonderful world of trigger leads. Here’s what’s really happening behind the scenes (and how you can stop it).

What Are Trigger Leads?

When you apply for a mortgage (or even a car loan or new credit card), the credit bureaus sell your info to other lenders. This is called a “trigger lead.” The only thing your lender shares is the credit pull—everything else, the bureaus already have.

How Credit Bureaus Sell Your Info

- Credit bureaus get a notification of your mortgage inquiry.

- They already have your contact info—no details from your lender.

- They sell your name, phone, email, and maybe address to “interested” lenders.

- Want out? Register with donotcall.gov—but it takes about 30 days.

Who’s Really Calling You?

- Anyone willing to pay for the list (often aggressive telemarketers, not legit lenders).

- They only know you’ve applied for a mortgage—not your rate, loan type, or lender.

- They’re NOT affiliated with me nor your mortgage company.

- They’re not trying to help you and theey dont have the best rates.

- Be cautious—don’t give out personal info to strangers.

Is It Legal?

Legislation to mostly ban trigger leads has passed Congress, but as of now, it’s not law. Until the President signs it, you’ll keep getting calls.

How to Stop Trigger Leads

- Register with donotcall.gov (National Do Not Call Registry)—allow up to 30 days.

- Report unwanted calls to the FCC and FTC.

- Save voicemails/texts—most callers don’t provide a legit company name or licensing info (that’s illegal, too).

- If calls persist and you’re curious, talk to a consumer protection attorney about your rights.

- Pro tip: A soft credit pull for pre-approval will NOT trigger these calls. If spam worries you, ask your lender about a soft pull until you’re on the Do Not Call list for 30 days.

Will This Affect Your Home Buying?

It’s annoying, but it shouldn’t stop you from buying a house or investing. The most important thing: don’t give sensitive info to anyone who cold-calls you. When in doubt, call your lender directly.

Final Tips & Resources

- Block numbers, don’t engage, and never click on strange links.

- Save evidence if you get repeated calls—report it to the FCC or FTC.

- Stay focused on your home goals. If you need help or want a safe, private pre-approval, let’s connect.

Ready to start your mortgage journey with less spam?

👉 Download my free Key Steps app and get tips to protect your info before you shop.